Zebra Technologies: Riding The Secular Growth Of Digital Supply Chains (NASDAQ:ZBRA)

Jae Young Ju

Introduction

The Zebra Technologies Corporation (NASDAQ:ZBRA) This company has been on my radar since many years. Despite its potential, the company has been under the radar. Zebra will benefit from an increase in supply chain investments. This is a new secular trend. Zebra’s wide range of products is a benefit as more supply chain businesses are expected to invest technology.

This article will explore these developments and show you why Zebra is an attractive investment, particularly during market downturns when there are buying opportunities.

Let’s get on with it!

Supply Chains & High-Tech

I was reading an interesting article the other day that highlighted major supply chain concerns and ways to improve supply chains.

A Deloitte study found that 74% (2000) of the article’s readers are women. Respondents plan to increase their technology investments by 2023. 90% of these companies plan to spend 24% more in 2023 than the previous year. This is a significant growth rate for an economy that has a high chance of falling into recession.

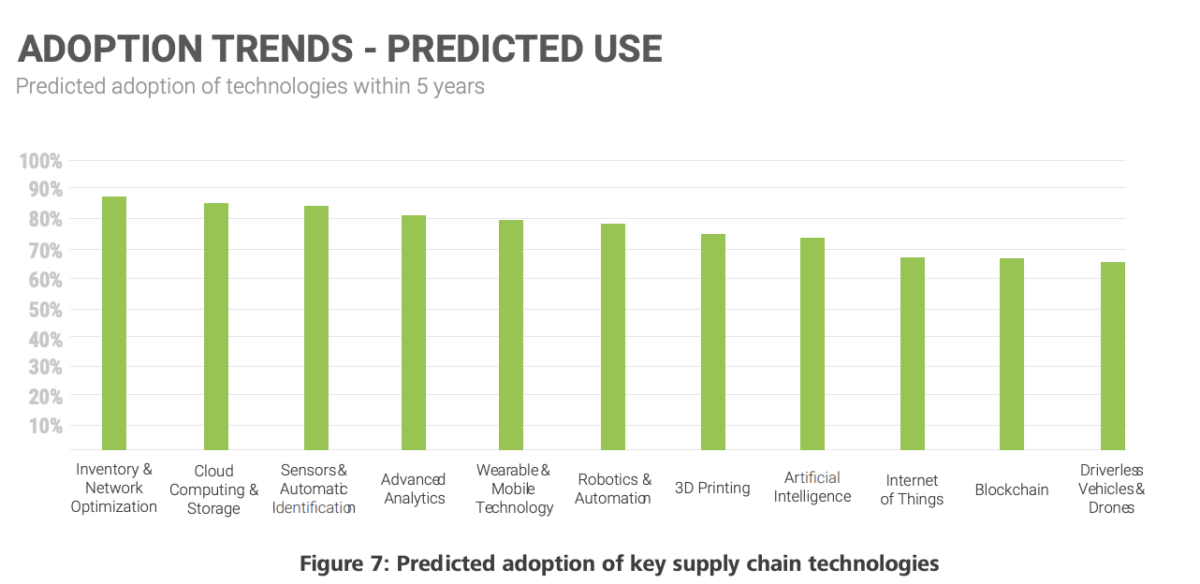

Inventory and network optimization are expected to be the most popular areas for technology adoption. 87% of respondents in this segment expect to significantly increase spending over the next five year.

This segment was followed by high expected growth in cloud computing, sensors & automatic identification, advanced analytics, and wearable & mobile technologies.

MHI, Deloitte

87% of respondents also believe supply chains will become autonomous, connected and intelligent by 2027. This is expected to make it the norm. Only 5% believe that the industry has reached this level today.

In the same survey, it was revealed that digital supply chains are expected to be the norm within the next ten-years. These digital supply chains will have end-to-end networks that allow transparency at all levels of execution and planning.

According to the report, companies who invest in digital transformation will experience increased speed, connectivity and transparency. They will also enjoy accurate, shareable and secure data that is actionable. This will transform the supply chain industry and companies who embrace this future will reap substantial rewards.

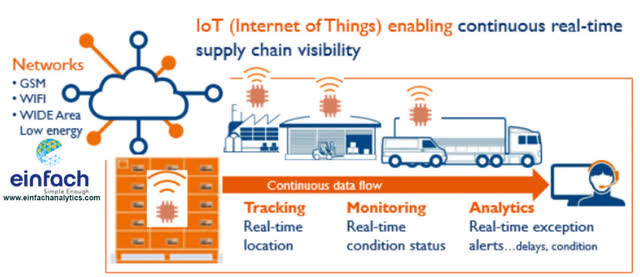

The report also highlighted the rapid pace at which supply chains are actually implementing the Internet of Things approach. This means that everything can be connected and allows for higher efficiency.

Zetes

Companies that successfully implement these technologies are more likely to succeed. Companies that are unable to adapt to these technologies will struggle and lose market share.

Because there is so much at stake, the spending on these technologies is high.

Zebra Technologies can help.

ZBRA: A great Supply Chain Tech Play

Zebra Technologies, a technology company, specializes in providing solutions and products for enterprise asset management and supply chain management. The company has a headquarters in Illinois, United States and is active in more than 100 other countries. Zebra products include mobile computers as well as barcode scanners and printers.

The company’s corporate website highlights its ability to modernize supply chain processes.

- Increase visibility to improve decision making

- The Internet of Things ecosystem is powered.

- Improve data insight

Zebra Technologies

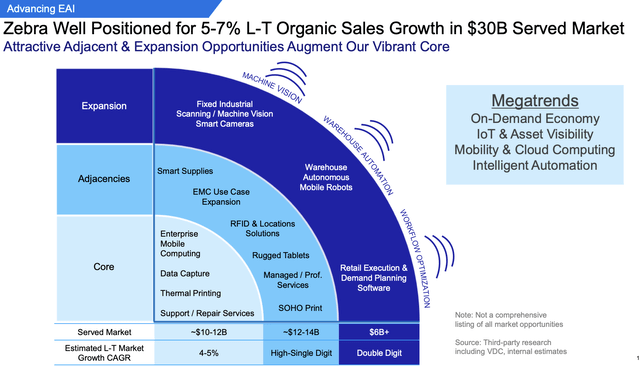

According to the 4Q22 earnings conference, the company made progress in its strategic relationship with customers. It also extended its leadership position in core businesses while gaining momentum in growth markets. The company provides comprehensive RFID solutions that can be used in a variety of applications and just won a record RFID deal. Zebra has also been gaining market share in rugged tablet markets as a result its focussed investment. Zebra believes it can deliver organic growth of 5% to 7 percent over a cycle with an increasing attractive margin profile.

Zebra Technologies

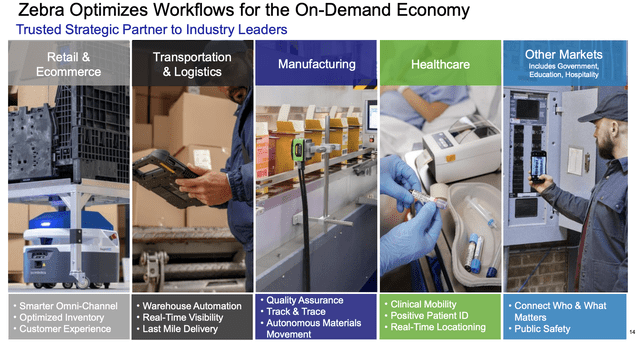

The company was able to address a broad range of workflows across different markets, including retail and ecommerce, transport logistics, manufacturing, health, and many other markets. Through its expanded offerings of solutions, including an autonomous mobile robot and machine-vision wins in manufacturing and warehouse use case cases, the company sees great opportunity to increase and grow customer relationships.

Zebra Technologies

Anders Gustafsson CEO highlighted the many achievements and the enormous value ZBRA brings to its clients when it comes down to serving them:

We were able to secure a number of important wins which helped us drive momentum into the future. These wins include a major Asian postal customer, who intends to improve productivity by equipping 70,000 of their mail carriers with our mobile computing solution. A British grocery store plans to increase their customer experience and improve their store efficiency by installing 80,000 personal shoppers devices. The European-based auto manufacturer intends to improve quality control and process improvement at all levels of production with 30,000 Zebra mobile computers.

This context suggests that Zebra is providing the right products for a fast increase in technology spending.

What about the Valuation

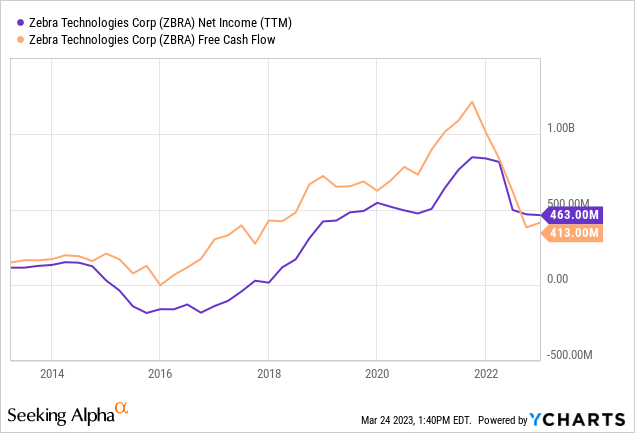

If we talk about growth stocks that are able to benefit from secular growth trends, it is often the case that we are dealing with money-losing companies that have yet to make a breakthrough. Zebra stock, however, is a consistently profitable company that has been in profit since 2018. This is also true for the free cash flow.

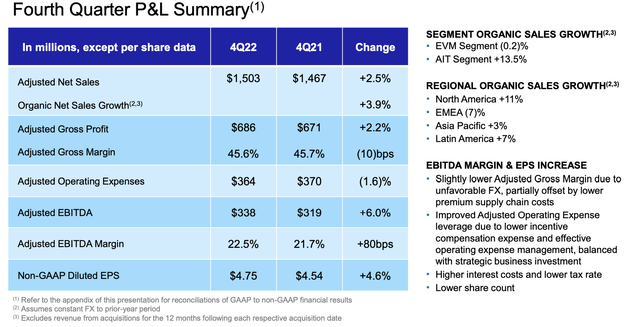

The company saw 3.9% organic growth in net sales in its latest quarter (4Q22), aided by 11% North America growth and 7% Latin America expansion. About half of the company’s revenues come from North America.

Zebra Technologies

With a 13.5% increase in sales, the Asset Intelligence & Tracking segment was ahead. This growth was driven by double-digit printing growth. Sales of the Enterprise Visibility and Mobility segments remained flat with different performance across offerings. Strong growth was seen in data capture solutions such as RFID and rugged tablets. However, mobile computing sales fell mainly because of difficult prior-year comparisons in EMEA. With strong service attach rates, the company saw significant growth in software and services.

EBITDA is expected to rise by 3.8% to $1.3Billion this year. The company’s growth for next year is $1.4 billion. This year’s free cash flow is expected at $690million. In 2024, it is expected to rise to $930million. This yields a 4.6% free cash flow yield in 2023E.

These growth rates include Matrox Imaging’s acquisition in 2022. The $880 million deal will add advanced hardware products as well as interoperable software capabilities.

The net debt is expected fall to $890million next year. This implies a net-leverage ratio lower than 1.0x EBITDA.

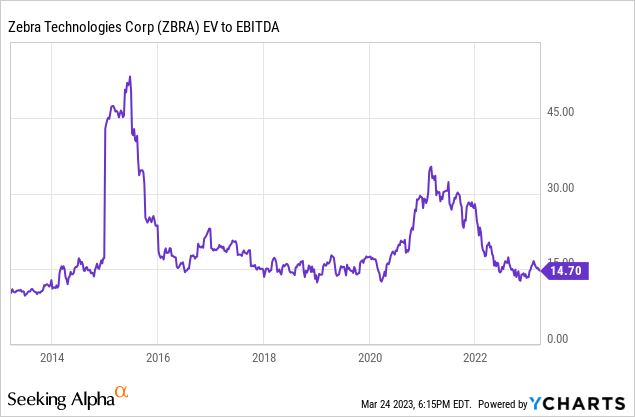

The company trades at 12.5x EBITDA using 2023 EBITDA numbers and net debt numbers. That number is 11.2x when you take 2024 numbers.

Given the company’s historic valuation at 14x EBITDA, which is fair, I consider the company’s fair value to range between $360 and $355. This means that there is roughly 30% opportunity for capital gains over the next 2 years. This conservative estimate is valid unless the economy plunges off a cliff. Current consensus estimates are $360. I am not far from that.

Takeaway

This article will focus on one of the most interesting companies in supply chain optimization. As investments in new-generation technologies increase, global supply chains are becoming more high-tech. Zebra Technologies is one such company. It’s well-respected in the right areas to assist companies in achieving their efficiency goals.

Zebra is gaining new customers quickly. It assists its clients in achieving their goals and is growing EBITDA and free liquidity rapidly. ZBRA, unlike other startups, has the ideal mix of growth and value. It also comes with an attractive valuation.

ZBRA shares are approximately 30% undervalued, despite economic weakness and market woes.